I am in denial

but I know children are dying

bilbo.economicoutlook.net (June 12 2010)

Governments around the world are being stampeded by financial commentators and international organisations (IMF, OECD, G-20) to implement austerity programs to get their "deficits under control". All sorts of horrendous predictions are being touted in the press daily by the deficit terrorists who focus their gaze on charts showing movements in financial ratios - such as the deficit to GDP and public debt to GDP ratios. They largely ignore history and when they do invoke it they introduce erroneous analyses which do not apply to the issue at hand. They erroneously conflate the Eurozone with sovereign monetary systems. And they never let up. But in all the talk of austerity the real dimensions of the problem get lost. That is what today's blog is about - getting our focus down to the fact that thousands of children will die as a result of these unnecessary austerity programs which are just designed to satisfy the ideological hangups of the (mostly) high income and wealthy elites in our societies.

The Editorial {1} in the New York Times on June 9 2010 was fairly to the point - The Wrong Message on Deficits. It said:

The Editorial notes that the "economic crisis isn't over" and cites the appalling unemployment that remains even though share markets have been recovering and some real economies are growing again, albeit slowly. They rightly conclude that "for everybody to slash public spending when growth is faltering and unemployment remains stubbornly high risks undercutting the goal of fiscal probity by slowing economic growth and reducing tax revenues".

And, they note that there is now evidence that the world economy is slowing again as the budget cuts take their toll. They conclude that:

Meanwhile, the Nikkei News for Thursday, June 10 2010 (you need a subscription so it is pointless to link) announced that DPJ's Fiscal Hawk Gets To Work As MOF Chief. The Report said that:

So it might be a case of Sayonara Japan ... it was nice knowing you! Back to 1997!

I also recall this article (June 9 2010) - The Dark Side Of Stimulus - by one Thomas Cooley, who is a retired academic from NYU and a regular Forbes columnist {2}. The article introduces a new term into the debate - deficit deniers.

Cooley notes that the recovery from the "deep recession" is not happening very quickly despite the "staggering ... fiscal package" that the US President introduced. He concludes that:

I am wondering who the we is who has to pay the bill. The bill is already being paid - the real loss of incomes and the persistently high unemployment. The only bill is a real one.

However, if governments insist on pretending they have to "finance" their spending and follow the path the UK is now taking (among other nations heading down the austerity path) then the real bill will be the lost real income arising from the cuts in public spending, the lost private command on real resources arising from the tax hikes. These costs will enormous.

Further, the only way of calibrating the worth of the fiscal interventions is to estimate outcomes such as "how many jobs were saved". We can roughly estimate the extra spending impact on GDP and hence employment growth. The important point is that in focusing on jobs we are displaying the appropriate priorities. In focusing on largely irrelevant aggregates such as the size of the deficit or the public debt ratio, we are exhibiting a wrong set of policy priorities.

Cooley notes that:

It is true that economic growth will reduce unemployment and, by definition, it increases incomes. But there is no robust empirical evidence that shows that rising deficits are associated with falling economic growth. The evidence points the other way. The fact that the US government has to honour the public debt is supportive of growth because the interest payments provide a higher income flow than if the funds were left in non-interest bearing reserves.

The Modern Monetary Theory (MMT) camp have been referring to the likes of Cooley as deficit terrorists. Cooley has his own term for those who think deficits are beneficial (when necessary):

MMT tells us that the size or continuity of budget deficits per se are not a sensible focus of analysis. The budget outcome is driven strongly by fluctuations in private spending. So a rising deficit usually indicates a slowdown in private spending. The discretionary component of the budget outcome should signal the extent to which the non-government sector desires to save (that is, withdraw spending from the income flow).

That spending gap has to be filled or else economic growth declines. There is no magic solution out there.

Further, while households may have taken advantage of low interest rates to over-borrow, that point is irrelevant to the question of public borrowing. There is no credible analogy between households (who use the currency) and a sovereign government (which issues the currency). The former are always revenue-constrained while the latter is never so.

The institutional structures that sovereign governments voluntarily erect to give the impression they are financially constrained are ultimately meaningless. They can be changed by the very government (in almost all cases) that they seek to "constrain". A sovereign government can always service its public debt obligations whereas a household cannot.

Cooley makes another fundamental error:

Whatever the international status of the US dollar is is irrelevant to the capacity of the US dollar to net spend in its own currency. All sovereign governments (who issue their own currency) can buy whatever is available for sale in their own currency at any time of their choosing. There is nothing special about the US government in this regard.

And ... all sovereign governments can purchase any idle labour in their economies and put it to productive use any time they choose to do so.

Cooley continues to misrepresent the monetary realities:

The high demand for US Treasuries certainly keeps the yields down given the way the auction system works. And the US dollar is seen as being a safe haven. But any sovereign government can engineer low public debt yields if it coordinates the central bank and treasury operations appropriately.

Cooley doesn't think this will last though because markets will eventually work out that the US deficit is not on "a sustainable fiscal path". To get there the US government has to "cut spending and increase revenues".

After drawing false analogies between the US and the fiscal plight of the Eurozone countries he says:

The stimulus has delivered less than imagined because they have been continually hamstrung by the deficit terrorists. In nations with the largest fiscal stimulus packages things are better. By introducing pressure on governments from the early stages of the crisis the terrorists have conspired to derail the recovery.

But then what would I know ... I am just in denial.

Anyway, this is just another one of the torrent of articles coming out which are pushing this line that austerity is needed and the larger and quicker the adjustment the better. But I have been reading some interesting research papers lately on the impacts of the stimulus packages and the likely impact of the austerity programs.

Fiscal stimulus proportions

UNICEF and other agencies have been doing work on the impact of the fiscal interventions, in particular the social protection measures that were introduced.

This UNDP paper - Social Protection in Fiscal Stimulus Packages: Some Evidence - by Zhang, Thelen and Rao {3}, found for the 35 countries studied, that, on average they:

So not a lot at all. They also found most of the social spending was on infrastructure and there was no real focus on women (and their children) who take the brunt of any economic crisis.

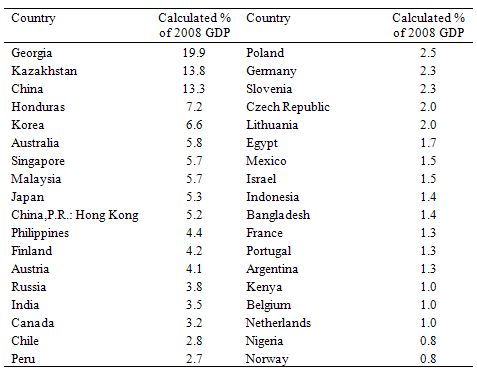

The following Table {4} is derived Table 1 in the UNDP paper referred to above. It shows the size of the fiscal stimulus as a percentage of 2008 GDP by the countries that the UNDP studied. I ranked them highest to lowest.

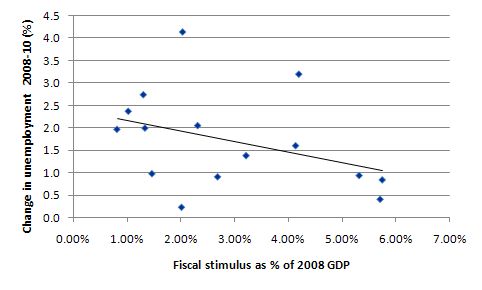

The point I have regularly made when confronted with claims like those outlined by Cooley - that the fiscal stimulus hasn't worked - is to note that the fiscal response has been relatively muted. They retort (shouting) asking whether I am blind - pointing to some public net spending ratio that has gone upwards. I reply that the ratios just tell me how deep the crisis has been.

I then say that the pools of unemployment tell me whether the fiscal response has been too much, just right or too little. And the unambiguous conclusion is that the fiscal responses have been inadequate by considerable margins.

The following graph {5} uses the data on the size of the fiscal stimulus as a percentage of 2008 GDP and plots the change in unemployment rates between 2008 and April 2010 against it. The data for the unemployment rates is from the World Economic Outlook database {6} as at April 2010. The plot only includes those nations for which the IMF published unemployment rates.

And while you don't want to conclude too much from a simple scatter plot, there appears to be the relationship emerging that theory would predict. The larger the stimulus the better the unemployment outcome. I am sure that a more thorough statistical analysis of this relationship controlling for other influences would confirm the simple message being portrayed in the graph.

The Losers

In all this talk about fiscal austerity - being pushed to make the bond traders happy - they who represent the wealthiest individuals in our societies - you will rarely read anything about who will be the beneficiaries and the losers.

We know from the privatisations of the 1980s and 1990s that spectacular transfers of wealth occurred. Governments paid huge sums to private financial organisations to execute the sales. Governments also agreed to heavy discounts on the true net worth and expected net income flows flows from the public enterprises being sold off because they didn't want the embarassment of a non-sale.

But who are the losers?

In its Global Economic Prospects 2010 {7}, the World Bank estimates that the global economic crisis pushed fifty million more people into extreme poverty in 2009 and a further 64 million will be added to this pool by the end of this year.

This paper - Crises and the Poor: Socially Responsible Macroeconomics {8} - by one Nora Lustig from the Inter-American Development Bank is worth reading to get an idea of how economic crises damage the prospects of the poor. It was written in 2000. While her documentation of the implications for crisis on the poor is interesting, I don't endorse her take on macroeconomics, which often wanders too far into the foibles of mainstream macroeconomics.

She does make on interesting point which is consistent with MMT. Lustig notes that "a flexible exchange rate" regime softens the blow of crises from a "pro-poor perspective". She notes that fixed exchange rate systems promote quantity adjustments to an external crisis (which in the labour market means unemployment) whereas flexible exchange system tends to make adjustments via real wages (import prices rise). In trying to defend a fixed parity, nations resort to harsh domestic policies which exacerbate poverty.

In this UNICEF paper - Inclusive Crises, Exclusive Recoveries, and Policies to Prevent a Double Whammy for the Poor {9} - Ronald Mendoza argues that:

You can read a lay-person summary {10} of the paper also.

While most of the research in this area of enquiry is focused on less developed (developing) nations, the research in advanced countries reveals similar outcomes. The poor are less exposed to crisis in the advanced nations and there are better safety nets.

But a person plunged into long-term unemployment in the US or Australia faces a high chance of becoming poor (relatively in this sense) and losing a significant proportion of the assets they had built up while working (housing, et cetera). Their children also inherit the disadvantage that they grew up with and face major difficulties in later life.

So it is not just a developing country problem - although in the poorer nations the impacts mean death in many cases. In poorer nations, a crisis has devastating impacts. Mendoza notes that "tens of thousands of children in some of the poorest countries in the world could die, paying the ultimate price as a result of this crisis".

But the recovery is also fraught for the poor.

Mendoza notes that:

This is the point that Lustig also emphasises.

The other point that Mendoza makes is that the meagre funds that:

You will rarely read anything like this is the daily financial debates about how much austerity to impose. While the erroneous construction of the monetary system by the deficit terrorists has an intellectual curiosity about it - that is, I wonder about motives, et cetera - the reality is much more important.

Even Mendoza thinks there is "an impending public finance crisis" sweeping the world. In general, there is no public finance crisis (Eurozone nations excluded). Sovereign nations should be focusing fiscal policy on improving domestic outcomes, in general, and ensuring, in particular, that the weak and vulnerable in their nations are protected. That is what public purpose is about.

If you just spend each day reading and debating at the level of the evening finance report then you will quickly lose sight of the human dimension of the crisis.

Mendoza's focus (in UNICEF) is on children and he says:

I was thinking about that statement in the context of the so-called intergenerational debate and the spurious arguments about transferring the burdens of public debt onto the next generation.

I have said it often but you cannot say it enough - the burden we are transferring to the future generation is the diminished opportunities they will have as a result of growing up in poverty. But it a burden that is also being borne now - every day - and manifests are malnutrition, lack of education and the other related pathologies that accompany poverty and social exclusion.

The austerity programs typically focus cuts in the areas where the poor are most reliant on public support.

Conclusion

Lustig says that:

Governments have a responsibility to use fiscal policy in a pro-poor manner and that "crisis prevention has to be a top priority of any anti-poverty strategy". This requires governments do not cut "pro-poor" programs during a crisis or in its aftermath. They should implement viable safety nets.

The Job Guarantee {11} is one such safety net and ensures that any person who can work and wants to work is able to access a socially-appropriate minimum wage at all times. This policy is the first thing any sovereign government should implement. The first policy that a non-sovereign government should implement is to make themselves sovereign, then introduce a Job Guarantee.

Governments should always use counter-cyclical net spending to advance social protection. Failure to do this not only impacts now but stifles human capital development in the future and thus ensures that poverty is transferred between generations.

Lustig says that:

So the New York Times editorial is largely correct (although they did say some nations should still implement austerity programs). No nation should implement discretionary cutbacks in net public spending at a time when the economy is in crisis. No exceptions!

But then I am just in denial - although I wonder how many children died today because of the crisis and the poor response by governments?

The Saturday Quiz will be back sometime tomorrow - even harder than last week!

That is enough for today!

Links:

{1} http://www.nytimes.com/2010/06/10/opinion/10thu1.html?hp

{2} http://www.forbes.com/2010/06/08/finance-economy-stimulus-anxiety-opinions-columnists-thomas-cooley.html?boxes=businesschannelsections

{3} http://www.undp.org/developmentstudies/docs/socialprotection_fiscalstimulus_march2010.pdf

{4} http://bilbo.economicoutlook.net/blog/wp-content/uploads/2010/06/Size_of_Stimulus_Table_2008_GDP.jpg

{5} http://bilbo.economicoutlook.net/blog/wp-content/uploads/2010/06/Fiscal_stimulus_change_UR_2008_2010.jpg

{6} http://www.imf.org/external/pubs/ft/weo/2010/01/weodata/download.aspx

{7} http://web.worldbank.org/WBSITE/EXTERNAL/EXTDEC/EXTDECPROSPECTS/GEPEXT/EXTGEP2010/0,,contentMDK:22438006~pagePK:64167689~piPK:64167673~theSitePK:6665253,00.html

{8} http://www.netamericas.net/researchpapers/documents/lustig/Lustig2.pdf

{9} http://www.unicef.org/socialpolicy/files/Inclusive_Crises_Exclusive_Recoveries.pdf

{10} http://voxeu.org/index.php?q=node/5157

{11} http://e1.newcastle.edu.au/coffee/job_guarantee/JobGuarantee.cfm

_____

This entry was posted on Friday, June 11th 2010 at 15:58 and is filed under Economics. You can follow any responses to this entry through the RSS 2.0 feed. You can skip to the end and leave a response. Pinging is currently not allowed.

http://bilbo.economicoutlook.net/blog/?p=10239

Bill Totten http://www.ashisuto.co.jp/english/

bilbo.economicoutlook.net (June 12 2010)

Governments around the world are being stampeded by financial commentators and international organisations (IMF, OECD, G-20) to implement austerity programs to get their "deficits under control". All sorts of horrendous predictions are being touted in the press daily by the deficit terrorists who focus their gaze on charts showing movements in financial ratios - such as the deficit to GDP and public debt to GDP ratios. They largely ignore history and when they do invoke it they introduce erroneous analyses which do not apply to the issue at hand. They erroneously conflate the Eurozone with sovereign monetary systems. And they never let up. But in all the talk of austerity the real dimensions of the problem get lost. That is what today's blog is about - getting our focus down to the fact that thousands of children will die as a result of these unnecessary austerity programs which are just designed to satisfy the ideological hangups of the (mostly) high income and wealthy elites in our societies.

The Editorial {1} in the New York Times on June 9 2010 was fairly to the point - The Wrong Message on Deficits. It said:

The whip-deficits-now fever is running hot on both sides of the Atlantic. In Europe, politicians are understandably spooked by investors dumping government bonds in the wake of the Greek meltdown. But the sudden fierce enthusiasm for fiscal austerity, especially among stronger economies, is likely to backfire, condemning Europe to years of stagnation or worse.

The United States is running the same very high risk. Democrats have soured on job creation and economic stimulus in favor of antideficit rhetoric, which Republicans have long seen as the easy road to discontented voters in a confusing election year.

The Editorial notes that the "economic crisis isn't over" and cites the appalling unemployment that remains even though share markets have been recovering and some real economies are growing again, albeit slowly. They rightly conclude that "for everybody to slash public spending when growth is faltering and unemployment remains stubbornly high risks undercutting the goal of fiscal probity by slowing economic growth and reducing tax revenues".

And, they note that there is now evidence that the world economy is slowing again as the budget cuts take their toll. They conclude that:

Right now, for the most robust economies - the United States, Germany, Britain, Japan - slashing budgets is the wrong thing to do.

Meanwhile, the Nikkei News for Thursday, June 10 2010 (you need a subscription so it is pointless to link) announced that DPJ's Fiscal Hawk Gets To Work As MOF Chief. The Report said that:

Yoshihiko Noda, the newly appointed chief of the Ministry of Finance, has long been considered one of the staunchest fiscal conservatives in the Democratic Party of Japan. Noda is eager to rebuild Japan's finances with a motto of "there should be no talk of policies without talk of funding sources". After the DPJ took power last September, Noda was named senior vice finance minister. He was front and center in cutting budget requests from ministries and agencies, rankling fellow DPJ lawmakers who formulated the requests.

So it might be a case of Sayonara Japan ... it was nice knowing you! Back to 1997!

I also recall this article (June 9 2010) - The Dark Side Of Stimulus - by one Thomas Cooley, who is a retired academic from NYU and a regular Forbes columnist {2}. The article introduces a new term into the debate - deficit deniers.

Cooley notes that the recovery from the "deep recession" is not happening very quickly despite the "staggering ... fiscal package" that the US President introduced. He concludes that:

But now people are realizing that there is a dark side to this spending orgy. It has to end, and then we have to pay the bill. If we need any reminders that the day of reckoning is coming we have only to look to Europe. There is no point in arguing about how many jobs have been created or saved by stimulus spending. We don't get to rerun history, so we won't know what the path of employment would have been absent the stimulus package.

I am wondering who the we is who has to pay the bill. The bill is already being paid - the real loss of incomes and the persistently high unemployment. The only bill is a real one.

However, if governments insist on pretending they have to "finance" their spending and follow the path the UK is now taking (among other nations heading down the austerity path) then the real bill will be the lost real income arising from the cuts in public spending, the lost private command on real resources arising from the tax hikes. These costs will enormous.

Further, the only way of calibrating the worth of the fiscal interventions is to estimate outcomes such as "how many jobs were saved". We can roughly estimate the extra spending impact on GDP and hence employment growth. The important point is that in focusing on jobs we are displaying the appropriate priorities. In focusing on largely irrelevant aggregates such as the size of the deficit or the public debt ratio, we are exhibiting a wrong set of policy priorities.

Cooley notes that:

... nothing will solve the problem except economic growth. The problem we face is that the extraordinary deficits we created are likely to restrain economic growth in the future. We do have to honor that debt.

It is true that economic growth will reduce unemployment and, by definition, it increases incomes. But there is no robust empirical evidence that shows that rising deficits are associated with falling economic growth. The evidence points the other way. The fact that the US government has to honour the public debt is supportive of growth because the interest payments provide a higher income flow than if the funds were left in non-interest bearing reserves.

The Modern Monetary Theory (MMT) camp have been referring to the likes of Cooley as deficit terrorists. Cooley has his own term for those who think deficits are beneficial (when necessary):

There are deficit deniers out there, like Paul Krugman, who think we can and should ignore deficits for a long time to come because we can continue to borrow at such low interest rates. This is the same behavior for which they excoriate households who accumulated too much mortgage and credit card debt. They also blasted Alan Greenspan and Ben Bernanke for enabling this irresponsible behavior by keeping interest rates too low for too long. But by all means let the Government borrow and spend at our current low interest rates to keep this economic recovery alive.

MMT tells us that the size or continuity of budget deficits per se are not a sensible focus of analysis. The budget outcome is driven strongly by fluctuations in private spending. So a rising deficit usually indicates a slowdown in private spending. The discretionary component of the budget outcome should signal the extent to which the non-government sector desires to save (that is, withdraw spending from the income flow).

That spending gap has to be filled or else economic growth declines. There is no magic solution out there.

Further, while households may have taken advantage of low interest rates to over-borrow, that point is irrelevant to the question of public borrowing. There is no credible analogy between households (who use the currency) and a sovereign government (which issues the currency). The former are always revenue-constrained while the latter is never so.

The institutional structures that sovereign governments voluntarily erect to give the impression they are financially constrained are ultimately meaningless. They can be changed by the very government (in almost all cases) that they seek to "constrain". A sovereign government can always service its public debt obligations whereas a household cannot.

Cooley makes another fundamental error:

There is certainly some truth to the view that we can kick the can down the road for a bit longer. Why? Because the US dollar is and will continue to be the world's reserve currency. It means that the US can run a persistent current account deficit because other countries need dollars for reserves.

Whatever the international status of the US dollar is is irrelevant to the capacity of the US dollar to net spend in its own currency. All sovereign governments (who issue their own currency) can buy whatever is available for sale in their own currency at any time of their choosing. There is nothing special about the US government in this regard.

And ... all sovereign governments can purchase any idle labour in their economies and put it to productive use any time they choose to do so.

Cooley continues to misrepresent the monetary realities:

This is also why we find it easy - even now with staggering deficits - to sell US Treasuries at low interest rates. Every time markets get shaky, as they have in recent weeks, there is a flight to the safety of US Treasury obligations. That reaffirms the belief in the long-term credibility of the US and the viability of our debt.

The high demand for US Treasuries certainly keeps the yields down given the way the auction system works. And the US dollar is seen as being a safe haven. But any sovereign government can engineer low public debt yields if it coordinates the central bank and treasury operations appropriately.

Cooley doesn't think this will last though because markets will eventually work out that the US deficit is not on "a sustainable fiscal path". To get there the US government has to "cut spending and increase revenues".

After drawing false analogies between the US and the fiscal plight of the Eurozone countries he says:

Markets and consumers are much smarter than politicians. That is why they are jittery. You don't have to be a rocket scientist to realize that the stimulus has not delivered the big bang people hoped for and that we can't afford more stimulus.

The stimulus has delivered less than imagined because they have been continually hamstrung by the deficit terrorists. In nations with the largest fiscal stimulus packages things are better. By introducing pressure on governments from the early stages of the crisis the terrorists have conspired to derail the recovery.

But then what would I know ... I am just in denial.

Anyway, this is just another one of the torrent of articles coming out which are pushing this line that austerity is needed and the larger and quicker the adjustment the better. But I have been reading some interesting research papers lately on the impacts of the stimulus packages and the likely impact of the austerity programs.

Fiscal stimulus proportions

UNICEF and other agencies have been doing work on the impact of the fiscal interventions, in particular the social protection measures that were introduced.

This UNDP paper - Social Protection in Fiscal Stimulus Packages: Some Evidence - by Zhang, Thelen and Rao {3}, found for the 35 countries studied, that, on average they:

... spend about 25% of their stimuli on social protection measures. In total, this amounts to about 653 billion US dollars, almost one percent of 2008 global GDP.

So not a lot at all. They also found most of the social spending was on infrastructure and there was no real focus on women (and their children) who take the brunt of any economic crisis.

The following Table {4} is derived Table 1 in the UNDP paper referred to above. It shows the size of the fiscal stimulus as a percentage of 2008 GDP by the countries that the UNDP studied. I ranked them highest to lowest.

The point I have regularly made when confronted with claims like those outlined by Cooley - that the fiscal stimulus hasn't worked - is to note that the fiscal response has been relatively muted. They retort (shouting) asking whether I am blind - pointing to some public net spending ratio that has gone upwards. I reply that the ratios just tell me how deep the crisis has been.

I then say that the pools of unemployment tell me whether the fiscal response has been too much, just right or too little. And the unambiguous conclusion is that the fiscal responses have been inadequate by considerable margins.

The following graph {5} uses the data on the size of the fiscal stimulus as a percentage of 2008 GDP and plots the change in unemployment rates between 2008 and April 2010 against it. The data for the unemployment rates is from the World Economic Outlook database {6} as at April 2010. The plot only includes those nations for which the IMF published unemployment rates.

And while you don't want to conclude too much from a simple scatter plot, there appears to be the relationship emerging that theory would predict. The larger the stimulus the better the unemployment outcome. I am sure that a more thorough statistical analysis of this relationship controlling for other influences would confirm the simple message being portrayed in the graph.

The Losers

In all this talk about fiscal austerity - being pushed to make the bond traders happy - they who represent the wealthiest individuals in our societies - you will rarely read anything about who will be the beneficiaries and the losers.

We know from the privatisations of the 1980s and 1990s that spectacular transfers of wealth occurred. Governments paid huge sums to private financial organisations to execute the sales. Governments also agreed to heavy discounts on the true net worth and expected net income flows flows from the public enterprises being sold off because they didn't want the embarassment of a non-sale.

But who are the losers?

In its Global Economic Prospects 2010 {7}, the World Bank estimates that the global economic crisis pushed fifty million more people into extreme poverty in 2009 and a further 64 million will be added to this pool by the end of this year.

This paper - Crises and the Poor: Socially Responsible Macroeconomics {8} - by one Nora Lustig from the Inter-American Development Bank is worth reading to get an idea of how economic crises damage the prospects of the poor. It was written in 2000. While her documentation of the implications for crisis on the poor is interesting, I don't endorse her take on macroeconomics, which often wanders too far into the foibles of mainstream macroeconomics.

She does make on interesting point which is consistent with MMT. Lustig notes that "a flexible exchange rate" regime softens the blow of crises from a "pro-poor perspective". She notes that fixed exchange rate systems promote quantity adjustments to an external crisis (which in the labour market means unemployment) whereas flexible exchange system tends to make adjustments via real wages (import prices rise). In trying to defend a fixed parity, nations resort to harsh domestic policies which exacerbate poverty.

In this UNICEF paper - Inclusive Crises, Exclusive Recoveries, and Policies to Prevent a Double Whammy for the Poor {9} - Ronald Mendoza argues that:

When it comes to aggregate economic shocks, the poor and the near-poor often face a double whammy. First, they are often among the most adversely affected by the shock, suffering from crisis effects that push them and their children (the next generation) deeper into poverty. Second, the poor and near-poor are also the least equipped to participate in and benefit from the subsequent recovery.

You can read a lay-person summary {10} of the paper also.

While most of the research in this area of enquiry is focused on less developed (developing) nations, the research in advanced countries reveals similar outcomes. The poor are less exposed to crisis in the advanced nations and there are better safety nets.

But a person plunged into long-term unemployment in the US or Australia faces a high chance of becoming poor (relatively in this sense) and losing a significant proportion of the assets they had built up while working (housing, et cetera). Their children also inherit the disadvantage that they grew up with and face major difficulties in later life.

So it is not just a developing country problem - although in the poorer nations the impacts mean death in many cases. In poorer nations, a crisis has devastating impacts. Mendoza notes that "tens of thousands of children in some of the poorest countries in the world could die, paying the ultimate price as a result of this crisis".

But the recovery is also fraught for the poor.

Mendoza notes that:

During a typical crisis episode, spending on the social sectors are often cut at precisely the time when these resources are needed the most. It is not uncommon that social spending suffers the largest cuts, and that part of social spending that has the greatest benefit for the poor is most retrenched ... we do know from past crises that families often have to sell off what little productive assets they might have, reduce health-seeking behaviour, pull children out of school, take on more debt, and in dire cases, eat less or less nutritious food in order to cope with the income shock. All these coping strategies hinder the ability of poor families to quickly recover.

This is the point that Lustig also emphasises.

The other point that Mendoza makes is that the meagre funds that:

... do allocate to the social sectors are now also at risk, as public budgets across the world are squeezed by declining tax and other revenues. If the food crisis, fuel crisis and financial crisis were the first three waves of crises - then the fourth wave is an impending public finance crisis now sweeping across developing and even some industrialised countries.

You will rarely read anything like this is the daily financial debates about how much austerity to impose. While the erroneous construction of the monetary system by the deficit terrorists has an intellectual curiosity about it - that is, I wonder about motives, et cetera - the reality is much more important.

Even Mendoza thinks there is "an impending public finance crisis" sweeping the world. In general, there is no public finance crisis (Eurozone nations excluded). Sovereign nations should be focusing fiscal policy on improving domestic outcomes, in general, and ensuring, in particular, that the weak and vulnerable in their nations are protected. That is what public purpose is about.

If you just spend each day reading and debating at the level of the evening finance report then you will quickly lose sight of the human dimension of the crisis.

Mendoza's focus (in UNICEF) is on children and he says:

Tomorrow's youth - today's children and infants - are at risk. Roughly about half of the developing world faces imminent or anticipated youth bulges within the next twenty years ... They are infants and children in some of the poorest countries today - many of the very same countries struggling to cope with the aftershocks of the food and fuel price crises, as well as the global slowdown.

Stock markets will bounce back; but children who miss an important window of nutrition, education, and care will shoulder the scars of the recent crises for the rest of their lives. Stronger social budgets, more nuanced and gender responsive policies, and where necessary support from the international community, could help to ensure that social and economic recovery from the most severe crises in recent history will be much more inclusive than in the past.

I was thinking about that statement in the context of the so-called intergenerational debate and the spurious arguments about transferring the burdens of public debt onto the next generation.

I have said it often but you cannot say it enough - the burden we are transferring to the future generation is the diminished opportunities they will have as a result of growing up in poverty. But it a burden that is also being borne now - every day - and manifests are malnutrition, lack of education and the other related pathologies that accompany poverty and social exclusion.

The austerity programs typically focus cuts in the areas where the poor are most reliant on public support.

Conclusion

Lustig says that:

Macroeconomic crises not only affect the current living standards of the poor, but their ability to grow out of poverty.

Governments have a responsibility to use fiscal policy in a pro-poor manner and that "crisis prevention has to be a top priority of any anti-poverty strategy". This requires governments do not cut "pro-poor" programs during a crisis or in its aftermath. They should implement viable safety nets.

The Job Guarantee {11} is one such safety net and ensures that any person who can work and wants to work is able to access a socially-appropriate minimum wage at all times. This policy is the first thing any sovereign government should implement. The first policy that a non-sovereign government should implement is to make themselves sovereign, then introduce a Job Guarantee.

Governments should always use counter-cyclical net spending to advance social protection. Failure to do this not only impacts now but stifles human capital development in the future and thus ensures that poverty is transferred between generations.

Lustig says that:

Permanent reduction in the stock of human capital of the poor, due to malnutrition and deteriorating skills, might also lead to lower economic growth. Socially responsible macroeconomic policy in crisis avoidance and crisis response can contribute simultaneously to lower chronic poverty and higher growth.

So the New York Times editorial is largely correct (although they did say some nations should still implement austerity programs). No nation should implement discretionary cutbacks in net public spending at a time when the economy is in crisis. No exceptions!

But then I am just in denial - although I wonder how many children died today because of the crisis and the poor response by governments?

The Saturday Quiz will be back sometime tomorrow - even harder than last week!

That is enough for today!

Links:

{1} http://www.nytimes.com/2010/06/10/opinion/10thu1.html?hp

{2} http://www.forbes.com/2010/06/08/finance-economy-stimulus-anxiety-opinions-columnists-thomas-cooley.html?boxes=businesschannelsections

{3} http://www.undp.org/developmentstudies/docs/socialprotection_fiscalstimulus_march2010.pdf

{4} http://bilbo.economicoutlook.net/blog/wp-content/uploads/2010/06/Size_of_Stimulus_Table_2008_GDP.jpg

{5} http://bilbo.economicoutlook.net/blog/wp-content/uploads/2010/06/Fiscal_stimulus_change_UR_2008_2010.jpg

{6} http://www.imf.org/external/pubs/ft/weo/2010/01/weodata/download.aspx

{7} http://web.worldbank.org/WBSITE/EXTERNAL/EXTDEC/EXTDECPROSPECTS/GEPEXT/EXTGEP2010/0,,contentMDK:22438006~pagePK:64167689~piPK:64167673~theSitePK:6665253,00.html

{8} http://www.netamericas.net/researchpapers/documents/lustig/Lustig2.pdf

{9} http://www.unicef.org/socialpolicy/files/Inclusive_Crises_Exclusive_Recoveries.pdf

{10} http://voxeu.org/index.php?q=node/5157

{11} http://e1.newcastle.edu.au/coffee/job_guarantee/JobGuarantee.cfm

_____

This entry was posted on Friday, June 11th 2010 at 15:58 and is filed under Economics. You can follow any responses to this entry through the RSS 2.0 feed. You can skip to the end and leave a response. Pinging is currently not allowed.

http://bilbo.economicoutlook.net/blog/?p=10239

Bill Totten http://www.ashisuto.co.jp/english/

posted by Bill Totten at

7:39 AM

![]()

![]()

{kind=link}

{kind=link}

0 Comments:

Post a Comment

<< Home